The Best Asset Distribution for Cryptocurrency Rebalancing

In our previous studies, all of the backtests were run with an even distribution of assets. This means if a portfolio of 5 cryptocurrencies was allocated, the selected allocation for each asset was 20%. During rebalances, each asset would be realigned to this allocation.

This study is putting distribution models to the test. We will examine 3 different distributions to determine the optimal allocation strategy. These allocation strategies will be the following:

Even

Linear

Exponential

Backtest Design & Setup

In order to evaluate each allocation strategy, we performed backtests over historic data. This allows us to create a simulation of how well a strategy would have performed in the past. The following constraints were used when performing each backtest.

Trades & Data

Market data was collected from May 4, 2017 to May 3, 2018. This data was used to calculate the price of trades as they would have happened at that time. The trading path between each asset was performed by first trading to BTC. This simplifies the path across exchanges which may have different base pairs. Each trade was simulated using a .25% trading fee.

All our data is available through the Shrimpy Historical Data API.

Assets & Initial Conditions

Every portfolio in this study consists of exactly 10 randomly selected assets. After each backtest, a new random group of 10 assets is selected for the next backtest. This process is completed 1,000 times for each strategy type and rebalance period. The complete list of assets which were included in the study can be found in our backtest tool.

At the start of each backtest, the portfolio is seeded with a $5,000 initial investment which is allocated across the assets. The rebalancing method used is outlined in our previous article.

A more in depth discussion of the backtest procedure and study setup can be found in our previous article:

Rebalance vs. HODL: A Technical Analysis

Even Allocation Distribution

This distribution follows an allocation of 10 percent for each asset.

Even distribution means that each asset holds the same weight in the portfolio. A portfolio of 10 assets would result in each asset holding exactly 10% weight in the portfolio. Whenever the portfolio is rebalanced, trades are made to realign the portfolio to match these desired allocations.

This group compares the performance of evenly distributed portfolios which contain 10 assets, but differ by rebalance period. Each histogram incorporates 1,000 backtests, where the x-axis is the value of a portfolio after 1 year which had an initial investment of $5,000. The y-axis is the number of backtests which fell into the portfolio value buckets that are defined on the x-axis. (Example: A backtest was run with a rebalance period of 1 hour and 10 evenly distributed assets in the portfolio. The results of a backtest was $200k after one year. This would mean you add a 1 to the bottom right chart in the x-axis bucket which has the range of $195k to $214k. This process is then repeated until 1,000 backtests have been run.)

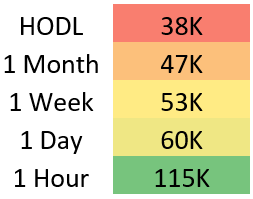

These values represent the median portfolio value in USD, 1 year after an initial investment of $5,000. Each value corresponds to their respective histogram displayed above.

Evenly distributed portfolios presented returns that ranged from a $40k median with HODL to a $123k median through rebalancing every hour. In addition to a higher median, rebalancing more frequently also presented a better spread. While the value of portfolios which used the HODL strategy were largely concentrated on the lower end, as observable in the above histograms, frequent rebalances improved the spread by distributing results over a wider range of values and higher performing portfolios. Not only did the median 1 hour rebalance period beat the median hodl, the worst performing portfolio out of over 1,000 backtests in the 1 hour rebalance strategy group beat the median HODL portfolio.

After 1 year, evenly distributed portfolios which rebalanced hourly had a return of 2,360%.

Linear Allocation Distribution

This distribution follows an allocation of 1, 3, 5, 7, 9, 11, 13, 15, 17, 19 percent for each asset.

Linear distributions still have a total sum of percentages that equal 100%, but the weights for each asset is uneven. The method in which they are uneven is linear. Since linear can have numerous meanings, we defined a portfolio with 10 assets to have a linear distribution of 1, 3, 5, 7, 9, 11, 13, 15, 17, 19 percent per asset. Whenever the portfolio is rebalanced, trades are made to realign the portfolio to match these desired allocations.

This group compares the performance of linearly distributed portfolios which contain 10 assets, but differ by rebalance period. Each histogram incorporates 1,000 backtests, where the x-axis is the value of a portfolio after 1 year which had an initial investment of $5,000. The y-axis is the number of backtests which fell into the portfolio value buckets that are defined on the x-axis. (Example: A backtest was run with a rebalance period of 1 hour and 10 linearly distributed assets in the portfolio. The results of a backtest was $200k after one year. This would mean you add a 1 to the bottom right chart in the x-axis bucket which has the range of $183k to $204k. This process is then repeated until 1,000 backtests have been run.)

These are the median portfolio values for each set of backtests which are detailed in the histograms above.

The results for a linear asset distribution presents a decline in returns over 1 year when compared to even distributions. The median values saw a decrease ranging from $2k for portfolios which used the HODL strategy, to $8k for portfolios which performed rebalances every 1 hour. We also see from the histograms that linear asset distributions decreased the spread of the results. Instead of a smooth curve, results aggregated at the lower end of this spread. This suggests that not only the median decreased, but there were also fewer high performing portfolios.

After 1 year, linearly distributed portfolios which rebalanced hourly had a return of 2,200%.

Exponential Allocation Distribution

This distribution follows an allocation of 1, 1, 2, 2, 4, 6, 9, 15, 23, 37 percent for each asset.

The final method of allocation distribution that we will discuss is the exponential distribution. This method simply allocates the assets in a way which results in one asset holding the lions share of the total portfolio value and each asset after that holds a fraction of the previous. We defined a portfolio with 10 assets to have a exponential distribution of 1, 1, 2, 2, 4, 6, 9, 15, 23, 37 percent per asset. Whenever the portfolio is rebalanced, trades are made to realign the portfolio to match these desired allocations.

The first reaction you may have when looking at this distribution chart is that it looks like the allocations for a crypto index fund that tracks the top 10 assets by market cap. This is true. The major difference is that a top 10 index is based on current market caps, so the allocation for each asset shifts over time. Our study used fixed allocations across the one year time period. While this seems like a small distinction, it may be an important one.

This group compares the performance of exponentially distributed portfolios which contain 10 assets, but differ by rebalance period. Each histogram incorporates 1,000 backtests, where the x-axis is the value of a portfolio after 1 year which had an initial investment of $5,000. The y-axis is the number of backtests which fell into the portfolio value buckets that are defined on the x-axis. (Example: A backtest was run with a rebalance period of 1 hour and 10 exponentially distributed assets in the portfolio. The results of a backtest was $200k after one year. This would mean you add a 1 to the bottom right chart in the x-axis bucket which has the range of $176k to $201k. This process is then repeated until 1,000 backtests have been run.)

These are the median portfolio values for each set of backtests which are detailed in the histograms above.

The results for an exponential asset distribution presented an even larger decline in returns over 1 year when compared to both even and linear distributions. The median values saw a decrease ranging from $3k for portfolios which used the HODL strategy, to $20k for portfolios which performed rebalances every 1 hour. We also see from the histograms that these backtests continued the trend of declining spread. The results are aggregated at the lower end of this spread, even more than the backtests which explored linear allocation distributions. This suggests both a decrease in median from the linear distribution, as well as a decrease in frequency of high earning portfolios.

After 1 year, linearly distributed portfolios which rebalanced hourly had a return of 1,760%.

Conclusions

Combining all of the results from this study, we can see how the median portfolio performed over the last year for each of these strategies and rebalance periods.

These are the median portfolio values for each set of backtests combined across all histograms which were detailed above. Each value represents 1,000 backtests. With a starting portfolio value of $5,000, these median values represent the final value held by the portfolio after 1 year.

This heat map indicates that even distributions with a 1 hour rebalance outperformed non-even distributions over the last year. In fact, the more uneven the distribution of funds, the worse the median portfolio performed.

Disclaimer: Backtests examine past performance and do not guarantee future performance.

Rebalancing with Shrimpy

The last year has proven that rebalancing a diverse portfolio can improve performance. Shrimpy simplifies the entire portfolio management and rebalancing process to a point and click interface. Quickly select assets, instantly allocate a diverse portfolio, and rebalance on a scheduled time period. Best of all, Shrimpy is easy to use!

Sign up by clicking here.

If you still aren’t sure, try out the demo to see everything we have to offer!

Additional Reading

Crypto Users who Diversify Perform Better

Evaluating Crypto Portfolio Performance Based On Asset Market Capitalization

Don’t forget to check out the Shrimpy website, follow us on Twitter and Facebook for updates, and ask any questions to our amazing, active communities on Telegram & Discord.

Leave a comment to let us know your experiences with Shrimpy!

The Shrimpy Team