This Bitcoin Trading Strategy Outperformed HODLing

The following study will evaluate the historical performance of a threshold rebalancing strategy on the Binance exchange. The goal of this study is to better understand how threshold rebalancing stacks up against other strategies like buy and hold (HODL) and periodic rebalancing. The results of this study can help us make better decisions during the portfolio construction process. Not only is it important to consider the assets which are included in any portfolio, but also the rebalancing strategy which you use to maintain your portfolio allocations.

Threshold rebalancing is a strategy which has recently emerged onto the cryptocurrency portfolio management scene when it was integrated into the Shrimpy application. In conjunction with other advanced settings, it provides a powerful set of portfolio management controls which haven’t been available anywhere else in the cryptocurrency market.

Read more about rebalancing here.

Don’t forget to join our Telegram group so you are always up to date with the most important cryptocurrency portfolio studies and news!

Study Setup

This study will evaluate both threshold rebalancing strategies ranging from 1% to 50% as well as periodic rebalancing strategies ranging from time periods of 1 hour to 1 month.

The following constraints were used when performing each backtest:

Trading Fee: .1% (Highest Fee for Binance Users)

Data: Exact bid-ask pricing data was collected directly from the Binance exchange.

Data Time Period: June 21, 2018 – June 21, 2019.

Portfolio Asset Distribution: Each asset is evenly weighted in the portfolio.

Trading Route: All trades are routed through BTC.

Asset Selection: Assets were randomly selected from the pool of available assets on Binance.

Initial Investment: A $5,000 initial investment was used for each backtest.

Number of backtests: Each threshold and rebalance period was examined with 1,000 backtests.

Threshold Rebalancing Strategy: The strategy use for threshold rebalancing is outlined here.

A detailed discussion on the backtesting procedure can be found in our previous study here:

The Best Threshold for Cryptocurrency Rebalancing Strategies

Results

In this study, we will evaluate 15 different rebalance settings. Beginning with a 1% threshold rebalance, we will systematically increase the threshold up until we reach a 50% threshold. After we have examined the threshold rebalancing results, we will investigate how periodic rebalancing compares to these results. This will be accomplished by running backtest for hourly, daily, weekly, and monthly rebalances.

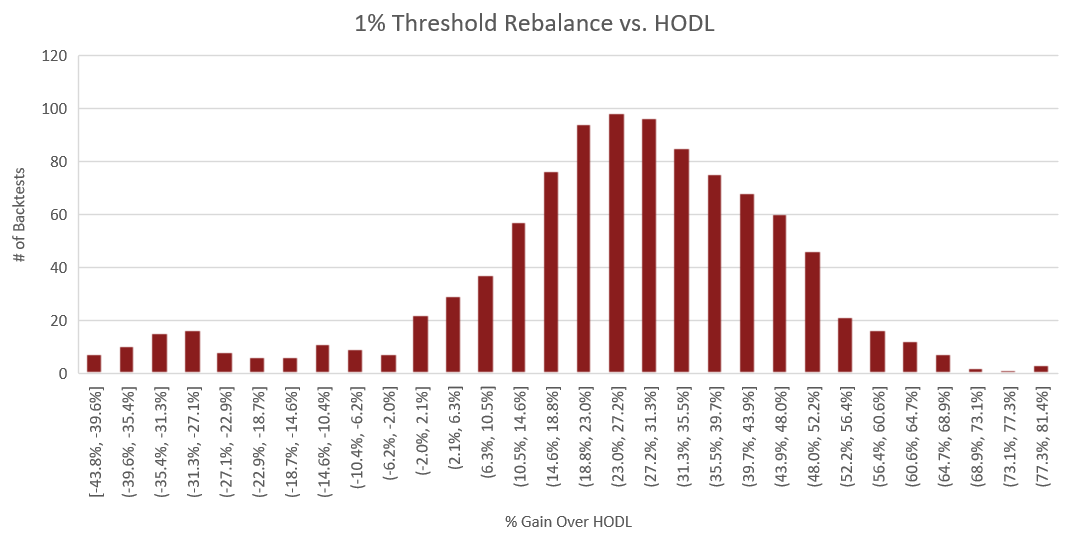

1% Threshold

Average Percent Performance Increase Over HODLing: 24.7%

Percent of Portfolios that Beat HODL: 89.7%

Median Percent Performance Increase Over HODLing: 26.9%

A 1% Threshold Rebalance Outperformed HODL by 26.9%

5% Threshold

Average Percent Performance Increase Over HODLing: 25.6%

Percent of Portfolios that Beat HODL: 88.9%

Median Percent Performance Increase Over HODLing: 28.6%

A 5% Threshold Rebalance Outperformed HODL by 28.6%

10% Threshold

Average Percent Performance Increase Over HODLing: 24.0%

Percent of Portfolios that Beat HODL: 89.6%

Median Percent Performance Increase Over HODLing: 26.5%

A 10% Threshold Rebalance Outperformed HODL by 26.5%

15% Threshold

Average Percent Performance Increase Over HODLing: 22.1%

Percent of Portfolios that Beat HODL: 88.8%

Median Percent Performance Increase Over HODLing: 25.1%

A 15% Threshold Rebalance Outperformed HODL by 25.1%

20% Threshold

Average Percent Performance Increase Over HODLing: 22.7%

Percent of Portfolios that Beat HODL: 90.1%

Median Percent Performance Increase Over HODLing: 25.4%

A 20% Threshold Rebalance Outperformed HODL by 25.4%

25% Threshold

Average Percent Performance Increase Over HODLing: 18.5%

Percent of Portfolios that Beat HODL: 86.2%

Median Percent Performance Increase Over HODLing: 21.3%

A 25% Threshold Rebalance Outperformed HODL by 21.3%

30% Threshold

Average Percent Performance Increase Over HODLing: 19.6%

Percent of Portfolios that Beat HODL: 86.9%

Median Percent Performance Increase Over HODLing: 22.1%

A 30% Threshold Rebalance Outperformed HODL by 22.1%

35% Threshold

Average Percent Performance Increase Over HODLing: 17.1%

Percent of Portfolios that Beat HODL: 86.3%

Median Percent Performance Increase Over HODLing: 20.3%

A 35% Threshold Rebalance Outperformed HODL by 20.3%

40% Threshold

Average Percent Performance Increase Over HODLing: 16.3%

Percent of Portfolios that Beat HODL: 85.4%

Median Percent Performance Increase Over HODLing: 18.6%

A 40% Threshold Rebalance Outperformed HODL by 18.6%

45% Threshold

Average Percent Performance Increase Over HODLing: 14.5%

Percent of Portfolios that Beat HODL: 83.5%

Median Percent Performance Increase Over HODLing: 16.7%

A 45% Threshold Rebalance Outperformed HODL by 16.7%

50% Threshold

Average Percent Performance Increase Over HODLing: 13.6%

Percent of Portfolios that Beat HODL: 83.4%

Median Percent Performance Increase Over HODLing: 16.1%

A 50% Threshold Rebalance Outperformed HODL by 16.1%

Hourly Periodic Rebalances

Average Percent Performance Increase Over HODLing: 22.4%

Percent of Portfolios that Beat HODL: 85.9%

Median Percent Performance Increase Over HODLing: 25.7%

A Hourly Rebalance Outperformed HODL by 25.7%

Daily Periodic Rebalances

Average Percent Performance Increase Over HODLing: 9.1%

Percent of Portfolios that Beat HODL: 79.3%

Median Percent Performance Increase Over HODLing: 13.0%

A Daily Rebalance Outperformed HODL by 13.0%

Weekly Periodic Rebalances

Average Percent Performance Increase Over HODLing: 1.9%

Percent of Portfolios that Beat HODL: 70.3%

Median Percent Performance Increase Over HODLing: 5.3%

A Weekly Rebalance Outperformed HODL by 5.3%

Monthly Periodic Rebalances

Average Percent Performance Increase Over HODLing: -1.0%

Percent of Portfolios that Beat HODL: 60.2%

Median Percent Performance Increase Over HODLing: 2.1%

A Monthly Rebalance Outperformed HODL by 2.1%

Overview

After running each set of backtests, we can combine the results to illustrate the median threshold rebalancing performance increase over buy and hold.

Graphing these median values over the various thresholds we examined shows the performance curve.

The performance curve graphed above demonstrates how the general trend for threshold rebalancing is that as we increase the threshold, the performance decreases. Therefore, we find that decreasing the threshold (increasing the rebalancing frequency) experiences an increase in performance.

Performance for threshold rebalancing on Binance peaks at a 5% threshold which experienced a 28.6% boost in performance over HODLing. As we increase the threshold percent, the performance increase over HODLed portfolios continues the downward trend. The lowest performance increase being a 16.1% increase for a 50% threshold.

To summarize these points in another format, the tables below break down the median performance increase for each of the rebalance strategies which were examined.

Figure 18: The above chart lists the median performance of threshold rebalancing at each of the corresponding percent thresholds.

Figure 17: The above chart graphs the median performance of periodic rebalancing at each of the corresponding rebalance periods.

Consistent with the results for threshold rebalancing, we find that periodic rebalancing on Binance peaks at a 1 hour rebalance period. This continues to suggest that higher frequency rebalancing has been more profitable for exchanges which have low trading fees and high liquidity. These results match previous studies which have been published on high frequency rebalancing.

Note: This data is specific to Binance. While high frequency rebalancing was found to increase performance in this study, our past studies which evaluated Bittrex data suggest executing frequent rebalances on less liquid exchanges with higher fees can result in decreased performance for the highest frequencies. You can find the study here.

Based on repeated results that threshold rebalancing has historically outperformed periodic rebalancing, we can begin to construct a case for threshold rebalancing as a valuable alternative to periodic rebalancing.

Some conceptual reasons for why threshold rebalancing may outperform periodic rebalancing include the following:

Threshold rebalancing can catch quick pumps due to the continuous monitoring of the market. Periodic rebalances do not react to the changes in the market between each rebalance.

Threshold rebalancing can reduce trading fees due to less frequent rebalances than periodic rebalances.

Threshold rebalancing will only trigger when the portfolio is misaligned from the target allocations. This means rebalancing will take place only when it’s necessary.

These points can help threshold rebalancing both reduce costs and increase returns over a long period of time.

Conclusions

Following these results, we find that threshold rebalancing considerably outperforms a simple buy and hold strategy over the examined time period. This observation is consistent with all our previous studies which have evaluated not only the performance of rebalancing strategies based on rebalancing frequency, but also the performance difference between exchanges which maintain varying levels of liquidity and trading fees. You can read each of these studies here:

The Best Threshold for Cryptocurrency Rebalancing Strategies

Exchange Liquidity: A Comparative Study

The results clearly show that a 5% threshold rebalancing strategy has outperformed all other strategies with a 28.6% increase over HODLing. The 5% threshold not only outperformed all other threshold rebalancing strategies, but also periodic rebalancing strategies.

A 5% Threshold Rebalance Outperformed HODL by 28.6%

Additional Reading

Automated Cryptocurrency Index Funds - Personal Asset Management

Portfolio Rebalancing for Cryptocurrency

Shrimpy is a trading bot and portfolio management application. Linking your Poloniex account to Shrimpy unlocks convenient trading features which can help you automate your crypto strategy. Try it out today!

Shrimpy’s Universal Crypto Exchange APIs are the only unified APIs for crypto exchanges that are specifically designed for application developers. Collect real-time trade or order book data, manage user exchange accounts, execute trading strategies, and simplify the way you connect to each exchange.

Follow us on Twitter and Facebook for updates, and ask any questions to our amazing, active communities on Telegram & Discord.

Leave a comment to let us know your experiences with threshold rebalancing!

The Shrimpy Team